The United States added 20.2 GW of new solar capacity in 2022, a 16% decrease from 2021. This was likely attributed to an investigation into new anti-circumvention tariffs by the U.S. Dept. of Commerce, as well as equipment detainments by Customs and Border Protection under the Uyghur Forced Labor Prevention Act.

Credit: Namaste Solar

According to the “U.S. Solar Market Insight 2022 Year in Review” released today by SEIA and Wood Mackenzie, utility-scale installations fell by 31% year-over-year to 11.8 GW, the sector’s lowest total since before the COVID-19 pandemic. Commercial and community solar installations also fell by 6% and 16%, respectively. Backlogs for connecting new solar projects to the electric grid continue to limit deployment in each market segment.

Projections for this and next year show a broad market recovery with growth across all sectors averaging 19% per year until 2027.

“Companies are aggressively shifting their supply chains, helping to ensure that solar installed in the U.S. is ethically sourced and has no connection to forced labor,” said SEIA president and CEO Abigail Ross Hopper. “While the solar and storage industry acts swiftly on supply chains and building a stronger domestic manufacturing base, ongoing threats of steep tariffs are holding back the potential of the historic Inflation Reduction Act.”

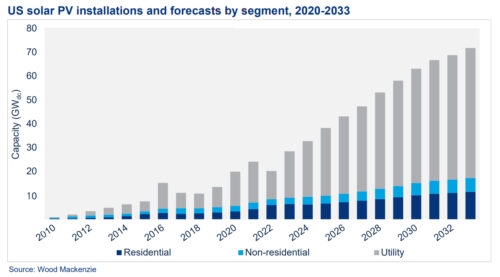

The report features updated 10-year baseline forecasts, along with high and low deployment scenarios based on solar module supply and domestic manufacturing, Inflation Reduction Act (IRA) guidance and sector-specific factors such as labor availability, tax equity supply and interconnection timelines.

The total difference between the high- and low-case outcomes amounts to 40 GW of new solar deployment in the next five years. In the base case, the United States is expected to add over 570 GW of new solar capacity in the next decade, bringing installed solar capacity from 141 GW today to over 700 GW in 2033.

“While 2022 was a tough year for the solar industry, we do expect some of the supply chain issues to ease, propelling 2023 growth to 41%,” said Michelle Davis, principal analyst at Wood Mackenzie and lead author of the report. “With major uncertainties ahead of the industry, our high- and low-case scenarios can help the industry benchmark potential outcomes. In each scenario, there is roughly 20 GW of upside or downside risk over the next five years — the same amount of capacity installed last year.”

The residential solar market experienced a 40% increase in installed solar capacity in 2022, and now 6% of all homes in the United States have solar. By 2030, that number is expected to grow to 15%.

In 2022, 783 MW of new residential, commercial and community solar capacity deployed was paired with energy storage systems, a new record. By 2027, 33% of new residential solar capacity and 20% of new commercial and community solar capacity will be paired with storage.

California, Texas, and Florida were the Top 3 states for new solar capacity additions for the third consecutive year, with California taking back the top spot after Texas led the nation in 2021.

Even as supply chain constraints slowed the market, solar accounted for 50% of all new electric generating capacity additions in 2022. Today, solar accounts for nearly 5% of U.S. electricity generation.