The solar PV industry is forecast to produce 310GW of modules in 2022, representing an incredible 45% year-on-year increase compared to 2021, according to the latest research undertaken by the PV Tech market research team and outlined in the new PV Manufacturing & Technology Quarterly report.

The market in 2022 was production-led and ultimately sized by the amount of polysilicon produced across the year. Demand at times likely ran 50-100% higher than what could be produced.

There will be enough polysilicon produced in 2022 to support the manufacturing of about 320GW of c-Si modules. Wafer and c-Si cell production levels are likely to end up around 315GW. Module production (c-Si and thin-film) should be close to 310GW, with final market shipments at 297GW. I am putting a ±2% error-bound on these values right now, with six weeks of production left for the year.

Of the 297GW of modules shipped in 2022, a significant amount of this will not result in new PV installation capacity. This is due to several factors; some standard, some new. Most pronounced have been the ‘stockpiling’ of modules at US customs and interconnection delays. But there is now certainly an appreciable volume going into module replacements or even plant repowering. Final new PV capacity added in 2022 may end up closer to 260GW once all of this is known fully.

From a manufacturing standpoint, there were no major surprises. China produced 90% of polysilicon, 99% of wafers, 91% of c-Si cells and 85% of c-Si modules. And of course, everyone wants domestic production, especially India, the US and Europe. Wanting is one thing; having is another.

About half of the polysilicon made in China during 2022 for the PV industry is produced in Xinjiang. This ratio will fall every year going forward now, with no new capacity expected to come online in this region.

In terms of technology, n-type made significant inroads, with TOPCon now the preferred architecture for the market leaders, although some fairly prominent names are hoping to drive through both heterojunction and back-contact to the multi-GW scale in 2023. Almost 20GW of n-type cells are forecast to be produced in 2022, of which 83% will be TOPCon. Chinese producers are driving the TOPCon transition; about 97% of TOPCon cells made in 2022 are in China. Next year will likely see this change, as TOPCon starts to find its way into the US utility segment, something that will demand TOPCon cells to be made outside China, maybe in Southeast Asia, but it does depend on what happens with ongoing investigations relating to anti-circumvention in the US.

In terms of module shipments during 2022, Europe turned out to be the big winner, although a staggering 100GW-plus of modules were made in China and kept in China. With the exception of the US, all other major end-markets saw strong double-digit growth, in keeping with the manic craving for solar that has gripped the world recently.

Europe was subject to a couple of issues in 2022 that caused the staggering growth seen. The region became the go-to shipment location for volumes that were not available to the US market and was also most immediately impacted by the consequences of the conflict in Ukraine. Almost 67GW of modules were shipped for the European market in 2022 – volumes no one was expecting a year ago.

Throughout the year, the PV industry was most visibly impacted by the new buzzword on everyone’s lips: traceability. Buying solar PV modules has never been so complicated.

Put aside the fact that pricing is still 20-30% higher than a couple of years ago, that contracts signed six months ago might not be worth the paper they are written on, or indeed the thorny topics of field reliability and honouring warranty claims.

Outranking all of these today is the traceability conundrum. Who makes what and where today, and more to the point, where will they make it in coming years.

The corporate world is grappling with this issue now and what it means when buying a PV module. I have written extensively on PV Tech over the past decade on why it is important to understand that most companies selling modules do nothing other than ‘package’ product made by other companies. Before, I thought it mattered mostly in terms of having confidence in quality; now this is being outranked by traceability and the need to audit supply chains.

Module buyers are having to take a crash course in manufacturing supply chain dynamics now, peeling off the layers of a module all the way back to the raw materials going into the polysilicon plants globally. Painful as it may seem, the final benefits will be significant, ultimately outranking that of traceability auditing.

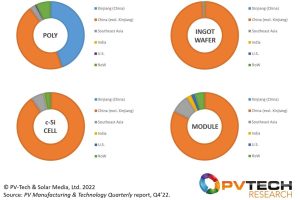

Right now, in terms of component production (polysilicon, wafer, cell and module) it is useful to segment the world into six parts: Xinjiang, the rest of China, Southeast Asia, India, the US, and the rest of the world. Maybe next year, Europe comes into play here, but for 2022 it is premature to pull out Europe (other than the fact that Wacker makes polysilicon in Germany).

The graphic below is taken from a webinar I delivered last week. It shows 2022 production across the various regions highlighted above.

China dominated manufacturing of PV components during 2022, with much of the focus on how much polysilicon was produced in Xinjiang.

China dominated manufacturing of PV components during 2022, with much of the focus on how much polysilicon was produced in Xinjiang.

Going into 2023, there are many uncertainties at this point, and I will try and cover these over the next couple of months at our events and in PV Tech features and webinars

While traceability and ESG will remain high on the agenda for most (both buying and selling modules), the issue of module price (ASP) could be the one to track most closely (again!).

Module ASP has remained high for a couple of years only because of this manic craving for solar that the net zero syndrome has imposed on governments, utilities and global corporates (solar remains the most attractive renewable energy due to speed of deployment and on-site/ownership flexibility). Even if one speculates that demand (undefinable when only a fraction of investors get product) for solar doubles in the next couple of years, at some point China capacity excess will enter the arena.

Simply put, if you want double something next year and the supply chain invests to make three times the volumes of last year, this becomes a buyer’s market and the price of the commodity comes down. Globally today, the bottleneck is polysilicon. In 2023, some markets may have other bottlenecks if there are import conditions imposed on other parts of the value chain (cells or modules, for example). But the focus is broadly on polysilicon and how much new capacity will come online in China and what this will produce; capacity and production are two very different things, especially when new players enter the space.

Forecasting polysilicon production in 2023 is very hard today. Not so much in terms of working out what level of new capacity will be ‘built’; more so in terms of what this will produce and if the Chinese polysilicon ‘cartel’ will act to control supply in order to keep it tight. It makes sense for the Chinese polysilicon producers to act as a club, or cartel, and slow down expansions if needed, or do extended maintenance mid-year to get through inventory.

History tells us the opposite though. Chinese companies tend to go overboard when there is a market need, and despite the country being ideally placed to pass down mandates on sector capacity levels, it does end up a free-for-all with endless money on the table for any new entrant with an industry aspiration.

It is important to note that polysilicon pricing can come down, but module pricing increase. This might be difficult to take in as it goes against normal logic within the PV industry. But it is something that may transpire in 2023. I will try and explain this now.

In a market with module oversupply (as the PV industry operated mostly until 2020), there tends to be downward module ASP trending and a squeeze upstream on costs. By default, polysilicon pricing (assuming oversupply there too) is low. Consider the sub US$10/kg back in the day.

During the past couple of years, module pricing did not go up simply because polysilicon supply was tight and the pricing increased (to above US$30/kg mostly), but because it was a module seller’s market. If polysilicon pricing in 2022 had decreased to US$10/kg, module suppliers could still have been able to sell product in the range 30-40c/W. There would just have been more margin for wafer, cell and module producers. You don’t bring a price down if you don’t need to.

For the past 18 months, it has been surprising to me that Beijing did not (completely behind the scenes) ‘order’ the polysilicon cartel in China to bring pricing down. Not to help the rest of the world when buying modules, but to allow a fairer share of the profits across the rest of the production value chain in China. I can only think it did not happen because everyone in China was able to prosper and keep 10-15% gross margins – even with polysilicon selling at US$40/kg. The only reason then for a Beijing edict would be to show the outside world that its polysilicon suppliers (remember half of China’s polysilicon in 2022 was made in Xinjiang) were not reporting 70-80% margins while under the spotlight arising from the whole Xinjiang question.

Therefore, it is not crazy that during 2023, there will be times that polysilicon pricing comes down but module pricing is unaffected and possibly even increases.

It is not all bad news for module buyers in 2023. There are signs that cyclical oversupply will occur, especially in the first half of 2023 and maybe being visible first for European module buyers. Much of this is coming from the fact that the Chinese sector is looking at shipping massive volumes to Europe and almost certainly way above what the European developers/EPCs can possibly make happen at short notice.

Most of these topics will be centre stage at the forthcoming PV ModuleTech conference in Malaga, Spain on 29-30 November 2022. There are still places available to attend the event; more information on the hyperlink here and how to register to attend. There has never been a better time for us to hold our first European PV ModuleTech conference!